RBI Bank Rate

RBI Bank Rate: Key Updates

Bank Rate Highlights – June MPC Meeting (Jun 3–5, 2026)

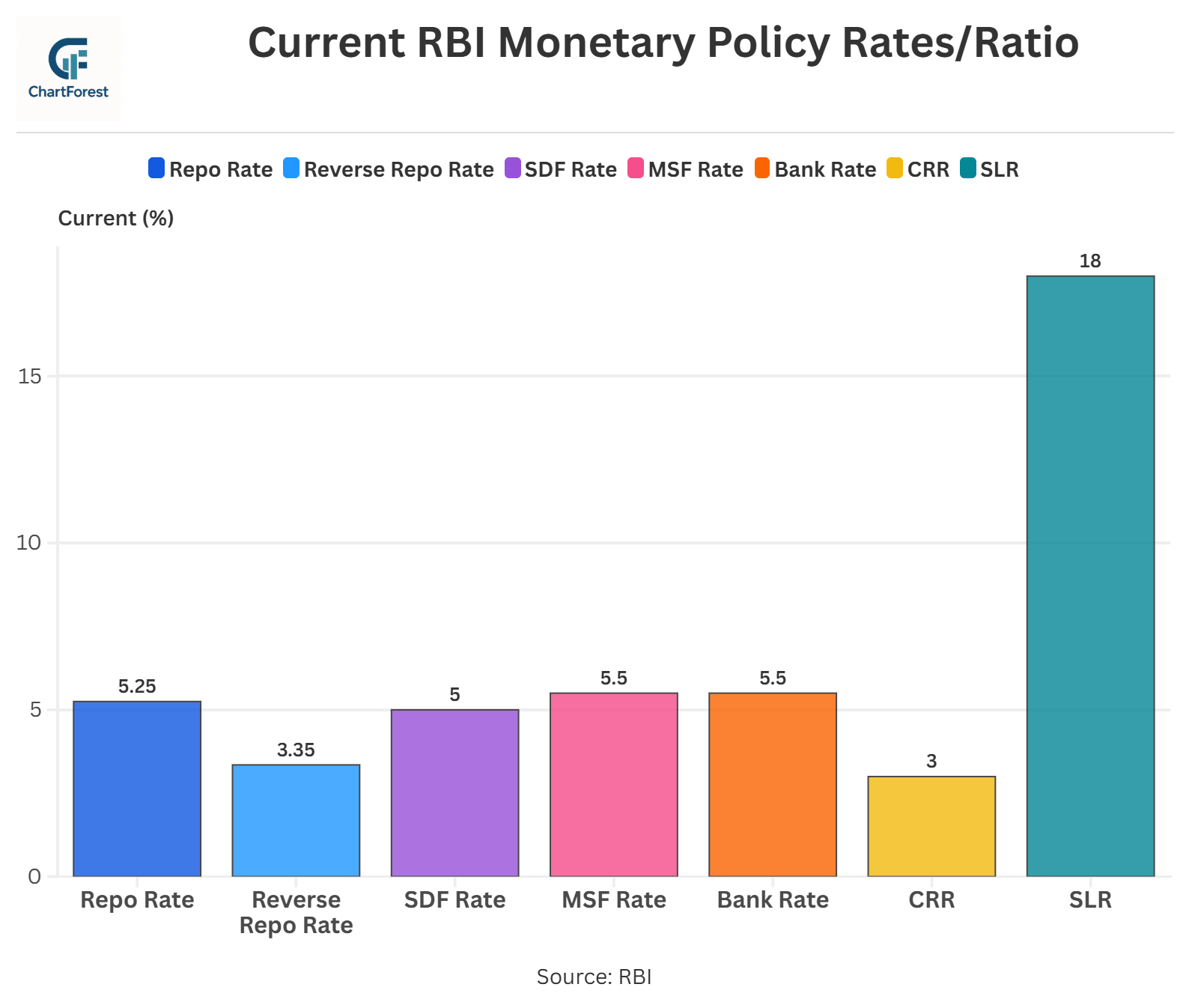

- The Monetary Policy Committee (MPC), at its 61st meeting held from June 3 to 5, 2026, kept the Bank Rate unchanged at 5.50%, in line with its decision to maintain the policy repo rate at 5.25%.

- The Bank Rate continues to move in alignment with the Marginal Standing Facility (MSF) rate, serving as an important reference rate for certain RBI lending operations and penal interest charges.

- The interest rate structure remains unchanged, with the Standing Deposit Facility (SDF) rate at 5.00%, the repo rate at 5.25%, and the MSF and Bank Rate at 5.50%, preserving the existing Liquidity Adjustment Facility (LAF) corridor.

- The Bank Rate remains a key component of the RBI’s monetary policy framework, helping maintain orderly liquidity conditions and ensuring effective transmission of policy signals across the financial system.

- The meeting was chaired by RBI Governor Shri Sanjay Malhotra, with members Dr Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr Poonam Gupta, and Shri Indranil Bhattacharyya in attendance.

- The MPC retained its neutral stance while highlighting increasing risks from elevated energy prices, global supply-chain disruptions, financial market volatility, and uncertainty arising from the prolonged West Asia conflict.

- The decision to keep the Bank Rate unchanged reflects the RBI’s cautious and data-dependent approach as it seeks to balance rising inflation risks with the need to support economic growth amid a challenging global environment.

Reasons for Maintaining the Bank Rate

Maintaining Consistency in the RBI’s Rate Framework: The Bank Rate is linked to the Marginal Standing Facility (MSF) rate and forms an important part of the RBI’s interest rate structure. Since the repo rate and MSF rate were left unchanged, maintaining the Bank Rate at 5.50% helps preserve consistency across the monetary policy framework.

Preserving the Existing Interest Rate Corridor: The RBI retained the SDF rate at 5.00%, the repo rate at 5.25%, and the MSF/Bank Rate at 5.50%. Keeping the Bank Rate unchanged ensures that the Liquidity Adjustment Facility (LAF) corridor remains intact, allowing short-term market rates to function within a predictable range.

Ensuring Smooth Monetary Policy Transmission: The Bank Rate serves as a reference rate for certain RBI operations and financial contracts. Maintaining it at the current level helps ensure that monetary policy signals continue to be transmitted smoothly through banks and financial institutions.

Avoiding Disruptions in Banking Operations: Changes in the Bank Rate can affect penal interest rates and certain borrowing arrangements linked to RBI facilities. By keeping the rate unchanged, the RBI avoids unnecessary disruptions to banking system operations and funding mechanisms.

Supporting Liquidity Management During Uncertain Times: Global uncertainties, volatile commodity prices, and financial market risks have increased the need for stable liquidity conditions. Maintaining the Bank Rate helps provide certainty to financial institutions while the RBI assesses evolving economic developments.

Allowing Time to Assess Inflationary Pressures: The RBI expects inflation to rise in the coming quarters due to higher fuel prices and supply-side pressures. Rather than making immediate adjustments to the Bank Rate, the MPC chose to monitor how these inflationary trends evolve before considering further action.

Balancing Financial Stability and Economic Growth: The Bank Rate plays an important role in the overall policy framework. Keeping it unchanged supports financial stability while allowing the RBI to balance inflation concerns with the need to support economic activity amid global headwinds.

Retaining Flexibility for Future Monetary Policy Actions: By maintaining the Bank Rate at 5.50%, the RBI preserves its ability to respond quickly to future changes in inflation, liquidity conditions, or economic growth. This aligns with the MPC’s data-dependent and neutral policy stance.

Expected Effects of the Unchanged Bank Rate

- Continuity in the RBI’s Monetary Framework: Keeping the Bank Rate unchanged at 5.50% reinforces stability within the RBI’s policy framework. Financial institutions can continue operating under a familiar interest rate structure without needing to adjust funding or compliance strategies.

- Stable Penal Interest Charges: Since the Bank Rate is used as a reference for certain penal interest rates and regulatory charges, maintaining the rate helps ensure that banks and financial institutions do not face unexpected increases in costs associated with regulatory non-compliance or shortfalls.

- Predictability for Financial Institutions: An unchanged Bank Rate provides greater certainty to banks when managing liquidity, capital, and funding requirements. Predictable policy settings help institutions focus on lending and business operations rather than adapting to sudden changes in the regulatory environment.

- Reinforcement of Policy Stability: The decision signals that the RBI is comfortable with the current policy corridor and liquidity conditions. This can strengthen confidence among market participants by demonstrating policy consistency during a period of elevated global uncertainty.

- Smooth Functioning of RBI Lending Facilities: The Bank Rate remains linked to certain RBI lending mechanisms and emergency funding arrangements. Keeping it unchanged ensures that these facilities continue to operate without disruption, supporting the overall stability of the banking system.

- Support for Financial Sector Confidence: Stable benchmark rates help create a predictable operating environment for banks, NBFCs, and other financial institutions. This can encourage orderly market behaviour and reduce uncertainty regarding future funding conditions.

- No Additional Pressure on the Banking System: An increase in the Bank Rate could have indirectly raised costs associated with RBI-linked facilities and regulatory penalties. By keeping the rate unchanged, the RBI avoids placing additional pressure on financial institutions at a time of growing external risks.

- Greater Flexibility as Economic Conditions Evolve: The unchanged Bank Rate allows the RBI to observe how inflation, growth, liquidity, and global developments unfold in the coming months. This provides policymakers with the flexibility to make more informed decisions in future monetary policy meetings.

Also Check: RBI Repo Rate Policy

RBI Bank Rate: Historical Chart

Bank Rate Chart (RBI) - Historical & Current Trends

RBI Monetary Policy Rates & Ratios

About RBI Bank Rate

Overview – The Bank Rate is the rate that is charged by the RBI (central bank) while giving loans to commercial banks. It provides a facility in which banks are not required to keep collateral with the RBI while borrowing money from it. Banks facing a shortage of funds can borrow from the central bank at this rate.

The RBI changes the bank rate after evaluating the economic conditions. The main purpose is to control inflation and stabilize the economy.

Bank Rate Change Impact

Increase Bank Rate: It makes borrowing expensive for banks and banks increase loan interest rates, making home, car, and business loans costlier. Moreover, this also helps control inflation by reducing excess money in circulation.

Decrease Bank Rate: It makes banks get cheaper loans from the RBI which makes loan interest rates for businesses and individuals decrease, encouraging them to borrow. Moreover, this helps boost economic growth during slowdowns.

FAQs

The bank rate is basically the interest rate the Reserve Bank of India (RBI) uses to lend long-term funds to commercial banks, and the best part is they don’t need to provide any collateral for it. It’s like a guiding rate for the financial system, helping to manage inflation and liquidity, and keeping the economy steady and balanced.

Both are lending rates set by the RBI, but the repo rate is meant for short-term borrowing, usually overnight, and requires collateral like government securities. The bank rate, however, applies to longer-term loans, doesn’t need collateral, and is typically higher than the repo rate, though it’s not used as often.

The RBI looks at a bunch of important factors like inflation trends, GDP growth, liquidity in the market, credit demand, and global economic signals to get a sense of how things are shaping up. Based on that, it tweaks the bank rate to either boost borrowing or ease it, helping keep the economy on the right track.

The bank rate plays a big role in shaping how banks borrow money, and it directly affects the economy. When the rate goes up, loans become more expensive, making borrowing tougher and slowing down inflation. On the flip side, when the rate drops, borrowing gets cheaper, which encourages spending, loans, and economic growth. In this way, the RBI uses the bank rate as a handy tool to manage liquidity, keep inflation in check, and steer overall economic activity.

Related Indicators

Other Indicators

Inflation and Price Indicators

GDP & Economic Growth Indicators

Trade & External Sector Indicators

Business & Industrial Indicators

Consumer & Labour Market Indicators

Important

If you notice any discrepancies in the data or find any inaccuracies, please let us know. We will review and correct them as soon as possible.