Cash Reserve Ratio (CRR)

RBI Cash Reserve Ratio (CRR): Key Updates

CRR Highlights – June MPC Meeting (Jun 3–5, 2026)

- At its 61st meeting held from June 3 to 5, 2026, the Monetary Policy Committee (MPC) did not announce any change to the Cash Reserve Ratio (CRR), leaving the reserve requirement for banks unchanged.

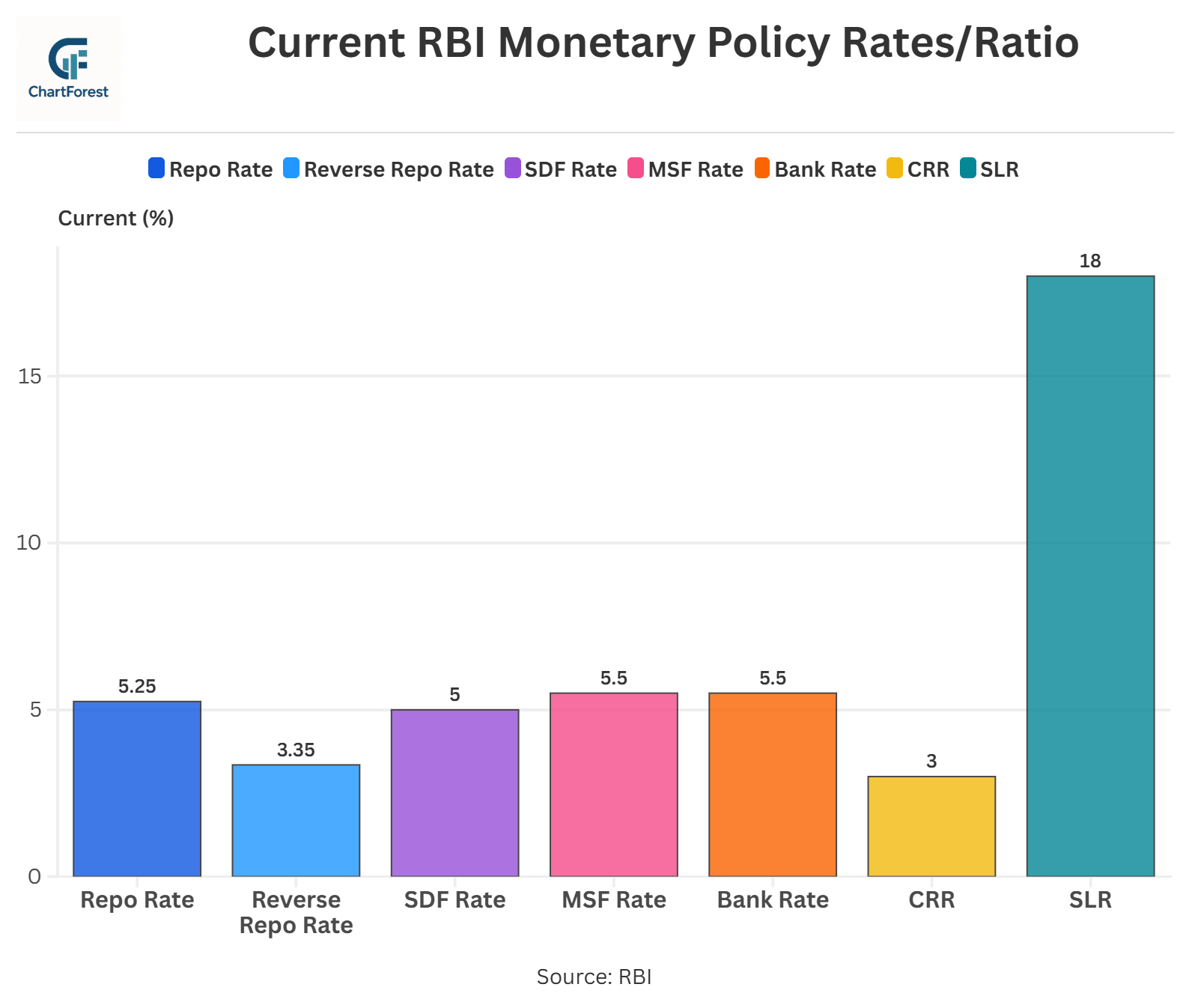

- The RBI’s policy focus remained on maintaining the repo rate at 5.25% and preserving overall monetary and financial stability amid increasing global and domestic uncertainties.

- By keeping the CRR unchanged, the RBI avoided injecting or withdrawing large amounts of liquidity from the banking system, helping maintain orderly liquidity conditions.

- The decision supports continuity in banking operations and allows financial institutions to plan their lending and liquidity management strategies without facing sudden reserve requirement changes.

- The CRR continues to serve as one of the RBI’s key structural liquidity management tools, complementing other instruments such as the Liquidity Adjustment Facility (LAF), open market operations (OMOs), and foreign exchange market operations.

- The meeting was chaired by RBI Governor Shri Sanjay Malhotra, with members Dr Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr Poonam Gupta, and Shri Indranil Bhattacharyya in attendance.

- The decision reflects the RBI’s cautious and data-dependent approach as it monitors rising inflation risks, global supply-chain disruptions, elevated energy prices, and the economic impact of the prolonged West Asia conflict.

- By maintaining the CRR, the RBI signalled its preference to keep liquidity conditions broadly stable while assessing how evolving inflation and growth dynamics affect the economy.

Reasons for Keeping CRR Unchanged

Maintaining Stable System Liquidity: The CRR directly affects the amount of funds banks can use for lending and investment. By keeping the CRR unchanged, the RBI avoided a sudden injection or withdrawal of liquidity from the banking system, helping maintain stable liquidity conditions.

Avoiding Disruptions to Bank Lending: A change in the CRR would immediately impact the amount of funds available with banks. Keeping the reserve requirement unchanged allows banks to continue supporting credit growth without facing unexpected liquidity adjustments.

No Immediate Need for Liquidity Tightening: Despite rising global uncertainties, the RBI did not see a need to absorb additional liquidity through a higher CRR. Existing liquidity management tools were considered sufficient to manage evolving financial conditions.

Using Other Liquidity Management Tools: The RBI has several instruments available to manage liquidity, including the Liquidity Adjustment Facility (LAF), open market operations (OMOs), variable rate auctions, and foreign exchange operations. As a result, changing the CRR was not considered necessary at this stage.

Monitoring Evolving Liquidity Conditions: The RBI is closely watching liquidity conditions amid global supply-chain disruptions, higher energy prices, and financial market volatility. Maintaining the CRR gives policymakers time to assess whether future liquidity adjustments may be required.

Focusing on Stability Rather Than Structural Changes: The June 2026 policy focused on maintaining stability in the financial system rather than making structural changes to reserve requirements. Keeping the CRR unchanged reflects the RBI’s preference for continuity while assessing emerging economic risks.

Expected Effects of the Unchanged CRR

- Lending Capacity of Banks Remains Intact: Since the CRR has been left unchanged, banks are not required to set aside any additional funds with the RBI. This allows them to continue using their existing resources for lending, investments, and other banking activities without disruption.

- No Sudden Liquidity Shock to the Banking System: Changes in the CRR can instantly add or remove large amounts of liquidity from the financial system. By maintaining the current CRR, the RBI has avoided creating sudden liquidity pressures that could affect banking operations and credit markets.

- Stable Credit Environment: An unchanged CRR helps ensure that the flow of credit to households, businesses, and industries remains broadly unaffected. Banks can continue their lending activities without adjusting to new reserve requirements.

- Better Balance Sheet Planning for Banks: Reserve requirements are an important factor in bank treasury and liquidity management. Keeping the CRR unchanged allows banks to plan their funding, asset allocation, and liquidity positions with greater certainty.

- Reduced Operational Adjustments: A CRR change often requires banks to recalibrate liquidity strategies and reserve management practices. The status quo reduces administrative and operational adjustments, allowing banks to focus on core business activities.

- Support for Deposit Mobilisation: Banks can continue managing their deposit base under existing reserve requirements. The absence of a CRR change helps maintain the current relationship between deposits, reserves, and lending activities.

- Liquidity Management Through Alternative Tools: The RBI can continue managing short-term liquidity using tools such as the Liquidity Adjustment Facility (LAF), variable rate operations, and open market operations, without relying on structural changes to reserve requirements.

- Greater Stability During Economic Uncertainty: At a time when global energy prices, supply-chain disruptions, and geopolitical tensions are creating uncertainty, an unchanged CRR provides stability to the banking system and helps prevent unnecessary disruptions in financial intermediation.

RBI Cash Reserve Ratio: Historical Chart

Cash Reserve Ratio (CRR) - Historical & Current Trends

RBI Monetary Policy Rates & Ratios

About RBI Cash Reserve Ratio (CRR)

Overview – CRR (Cash Reserve Ratio) is the percentage of a bank’s total deposits that the bank must keep as cash with the RBI. This money cannot be used for lending or investment purposes. To manage money supply, inflation, and liquidity in the Indian economy, the RBI uses CRR.

RBI’s Cash Reserve Ratio (CRR) Change Impact –

Higher CRR means > Banks have less money to lend > Less liquidity in the economy > Helps control inflation.

Lower CRR means > Banks have more money to lend > More liquidity in the economy > Encourages borrowing and boosts economic growth.

In short, when CRR increases, banks try to attract deposits from people, but loan growth also gets affected. On the other hand, when CRR decreases, banks try to encourage people and businesses to take loans, and it also helps boost the growth.

FAQs

The Cash Reserve Ratio (CRR) is basically the portion of a bank’s total deposits that it has to set aside as cash with the RBI. Banks aren’t allowed to use this amount for lending or investments. It’s one of the ways the RBI keeps a check on the money supply, inflation, and liquidity in India’s economy.

CRR is the portion of cash that banks are required to keep with the RBI, and they don’t earn any interest on it. On the other hand, SLR is a reserve that banks maintain in the form of approved securities, like government bonds or gold, which can earn them returns. While CRR helps control liquidity, SLR plays a role in ensuring the bank’s stability and solvency.

CRR has two key roles: it helps keep a portion of bank deposits safely with the RBI to safeguard depositors’ money, and it works as a handy tool for managing liquidity and keeping inflation in check.

When the CRR goes up, banks have less money to lend, which helps keep inflation in check by reducing the money supply. On the flip side, lowering the CRR gives banks more room to lend, potentially boosting economic growth, though it’s important to keep an eye on it since it could also raise inflation if not carefully managed.

CRR is essentially a fixed portion of a bank’s Net Demand and Time Liabilities (NDTL), which includes money from savings, current, and fixed accounts. It’s calculated using a simple formula: CRR = CRR rate (%) × NDTL.

Related Indicators

Other Indicators

Inflation and Price Indicators

GDP & Economic Growth Indicators

Trade & External Sector Indicators

Business & Industrial Indicators

Consumer & Labour Market Indicators

Important

If you notice any discrepancies in the data or find any inaccuracies, please let us know. We will review and correct them as soon as possible.