RBI Repo Rate Policy

RBI Repo Rate: Key Updates

Repo Rate Highlights: June MPC Meeting (Jun 3–5, 2026)

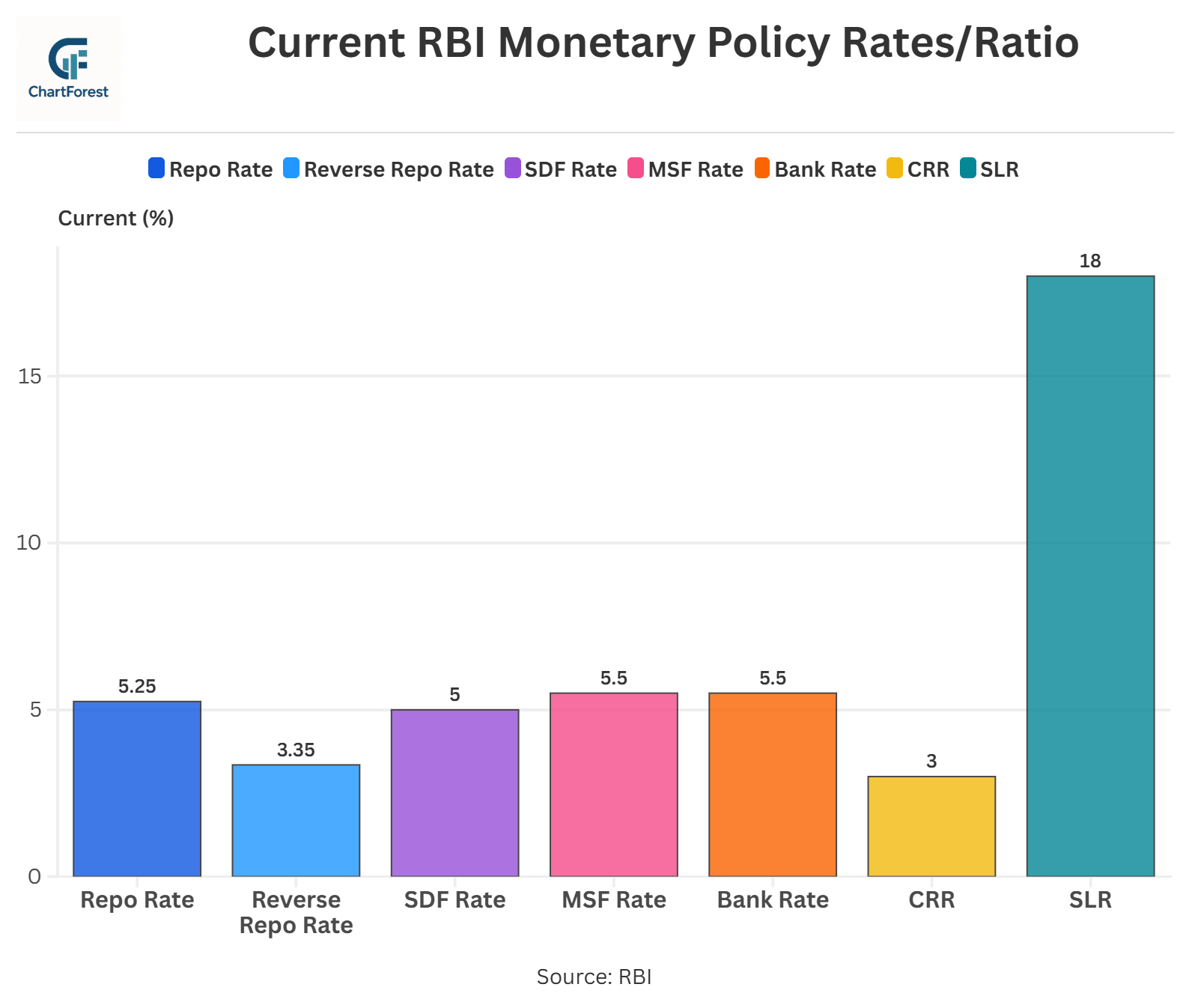

- The Monetary Policy Committee (MPC), at its 61st meeting held from June 3-5, 2026, voted unanimously to keep the policy repo rate unchanged at 5.25%.

- Consequently:

- Standing Deposit Facility (SDF) rate: 5.00%

- Marginal Standing Facility (MSF) rate: 5.50%

- Bank Rate: 5.50%

- The MPC decided to continue with the neutral stance, maintaining flexibility to respond to evolving economic and financial conditions.

- The meeting was chaired by RBI Governor Shri Sanjay Malhotra, with members Dr Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr Poonam Gupta, and Shri Indranil Bhattacharyya in attendance.

- Headline CPI inflation increased to 3.5% in April 2026, mainly due to higher food inflation, while core inflation remained stable at 3.7%.

- Real GDP growth for FY 2026-27 is projected at 6.6%, lower than the 6.9% projected in the April policy, reflecting rising global uncertainties and supply-side challenges.

- CPI inflation for FY 2026-27 is projected at 5.1%, higher than the 4.6% forecast in April, due to rising energy prices, supply-chain disruptions, and potential weather-related risks.

- The RBI highlighted increasing risks from the prolonged West Asia conflict, elevated crude oil and commodity prices, global supply-chain disruptions, financial market volatility, and a forecast of a deficient southwest monsoon.

- Domestic demand remains resilient, supported by private consumption, government capital expenditure, strong credit growth, and steady services sector activity, although signs of moderation are emerging in some sectors.

- The MPC emphasised a cautious and data-dependent approach, noting that inflation risks have increased significantly while growth prospects face downside pressures. The committee decided to keep rates unchanged until greater clarity emerges on global developments, supply chains, and inflation dynamics.

Reasons for Holding the Repo Rate

Rising Inflation Risks

- Inflation risks have increased due to rising crude oil and commodity prices caused by the prolonged West Asia conflict.

- CPI inflation is projected at 5.1% for FY 2026–27, higher than the RBI’s previous forecast.

- Higher fuel prices and increased input costs could lead to broader inflationary pressures across the economy.

Global Uncertainty and Supply Chain Disruptions

- Ongoing geopolitical tensions have disrupted global supply chains and increased uncertainty for businesses and policymakers.

- Volatility in global financial markets and changing interest rate expectations among major central banks continue to pose risks.

- The RBI is closely monitoring the impact of these developments on India’s economic outlook.

Weather-Related Concerns

- The forecast of a deficient southwest monsoon could affect agricultural output and rural demand.

- Potential El Niño conditions may put upward pressure on food prices and increase inflation risks.

Growth Outlook Remains Mixed

- Domestic demand remains resilient, supported by private consumption, investment activity, and government capital expenditure.

- However, elevated energy prices, higher logistics costs, and weaker global demand could slow economic growth.

- The RBI lowered its FY 2026-27 GDP growth forecast to 6.6%, reflecting these emerging challenges.

Need for a Cautious Approach

- The MPC believes it is prudent to wait for greater clarity on the duration and impact of global disruptions.

- Keeping the repo rate unchanged allows the RBI to balance inflation control with supporting economic growth.

- The committee will remain data-dependent and continue to assess incoming economic and inflation data before taking further policy action.

Maintaining Policy Flexibility

- By retaining the repo rate at 5.25% and maintaining a neutral stance, the RBI preserves flexibility to respond to future economic developments.

- The MPC remains prepared to act if inflationary pressures intensify or growth conditions weaken significantly.

Expected Effects of the Repo Rate Hold

- Borrowing Costs Remain Stable: With the repo rate unchanged at 5.25%, banks are unlikely to make immediate changes to their lending rates. As a result, EMIs on home loans, vehicle loans, and other retail loans are expected to remain broadly stable, providing relief to borrowers.

- Support for Economic Growth: Stable interest rates help maintain consumer spending and business investment. By avoiding a rate hike, the RBI aims to support economic activity at a time when global uncertainties and supply-chain disruptions are creating headwinds for growth.

- Inflation Remains Under Watch: Although the RBI has kept rates unchanged, inflation risks have increased due to higher energy prices, supply disruptions, and monsoon-related concerns. The central bank will continue to closely monitor price trends and inflation expectations.

- Positive for Credit Growth: A stable interest rate environment is expected to support continued growth in bank lending. Businesses and households may remain more willing to borrow, helping sustain demand for credit across various sectors of the economy.

- Relief for Financial Markets: The decision provides certainty to investors during a period of heightened global uncertainty. Stable policy rates can help reduce market volatility and support investor confidence in both equity and debt markets.

- Support for Household Finances: By keeping borrowing costs unchanged, the RBI has avoided adding pressure on household budgets. Consumers can continue managing their finances without facing an immediate increase in loan repayment obligations.

- Flexibility for Future Policy Action: Maintaining the neutral stance gives the RBI flexibility to respond to future economic developments. Depending on how inflation and growth evolve, the central bank can either tighten or ease monetary policy in upcoming meetings.

- Balanced Approach to Growth and Inflation: The repo rate hold reflects the RBI’s attempt to balance inflation control with economic growth. With risks to both inflation and growth increasing, the MPC has chosen a cautious approach while awaiting greater clarity on global and domestic conditions.

Overall, the RBI has adopted a cautious and data-dependent approach, choosing to keep the repo rate unchanged while closely monitoring evolving inflation and growth dynamics. With rising global uncertainties, higher energy prices, supply-chain disruptions, and monsoon-related risks, the MPC believes it is prudent to wait for greater clarity before taking further policy action.

Also Check: Standing Deposit Facility (SDF) Rate

RBI Repo Rate: Historical Chart

Repo Rate Chart (RBI) - Historical & Current Trends

RBI Monetary Policy Rates & Ratios

About RBI Repo Rate

Overview – Repo Rate is the interest rate at which the Reserve Bank of India (RBI) lends money to commercial banks (both govt and private) when they need funds.

So, how does the Repo Rate work?

When banks need money, they approach the RBI and borrow by using govt securities as collateral. They (banks) pay interest (according to the repo rate) on the borrowed amount to the RBI. Therefore, when the repo rate changes, it affects loan interest rates, inflation, and economic growth.

RBI Repo Rate Change Impact

What happens when RBI cuts the Repo Rate:

- Banks can borrow money more easily from the RBI.

- Loan interest rates drop, and it makes borrowing cheaper for consumers.

- More and more people take loans, increasing spending and stimulating the economy.

What happens when RBI increases the Repo Rate:

- Banks pay more to borrow from the RBI, making loans expensive.

- Fewer people take loans, reducing the money supply in the market.

- Helps control inflation by slowing down excessive spending.

FAQs

The Repo Rate is basically the interest rate the RBI charges when lending money to banks for a short time. To make this happen, banks hand over government-approved securities as collateral, with an agreement to repurchase them later. It’s a handy way for banks to cover their short-term cash needs.

The Repo Rate is essentially what commercial banks pay to borrow money from the RBI, while the reverse repo rate is what they earn when they deposit extra funds with the RBI. Usually, the repo rate is higher than the reverse repo rate.

Loans tied to the repo rate are closely connected to changes in the RBI’s benchmark lending rate. When the repo rate drops, it’s good news for borrowers—it often means banks will lower their lending rates, which could bring down interest rates and make your monthly EMIs a bit lighter. On the flip side, if the repo rate climbs higher, those with repo-linked loans might see their interest rates and EMIs go up faster than loans tied to other benchmarks.

When repo rates are higher, it can cool down business growth and squeeze company profits, which might put some pressure on the stock market. On the flip side, lower rates make borrowing simpler, often giving the market a nice little boost.

The RBI tweaks the repo rate to keep inflation in check and guide the flow of money in the economy. When the rate goes up, it helps cool off spending to manage inflation, and when it’s lowered, it nudges borrowing and boosts growth.

Related Indicators

Other Indicators

Inflation and Price Indicators

GDP & Economic Growth Indicators

Trade & External Sector Indicators

Business & Industrial Indicators

Consumer & Labour Market Indicators

Important

If you notice any discrepancies in the data or find any inaccuracies, please let us know. We will review and correct them as soon as possible.