RBI Statutory Liquidity Ratio (SLR)

RBI Statutory Liquidity Ratio (SLR): Key Updates

SLR Highlights: June MPC Meeting (Jun 3–5, 2026)

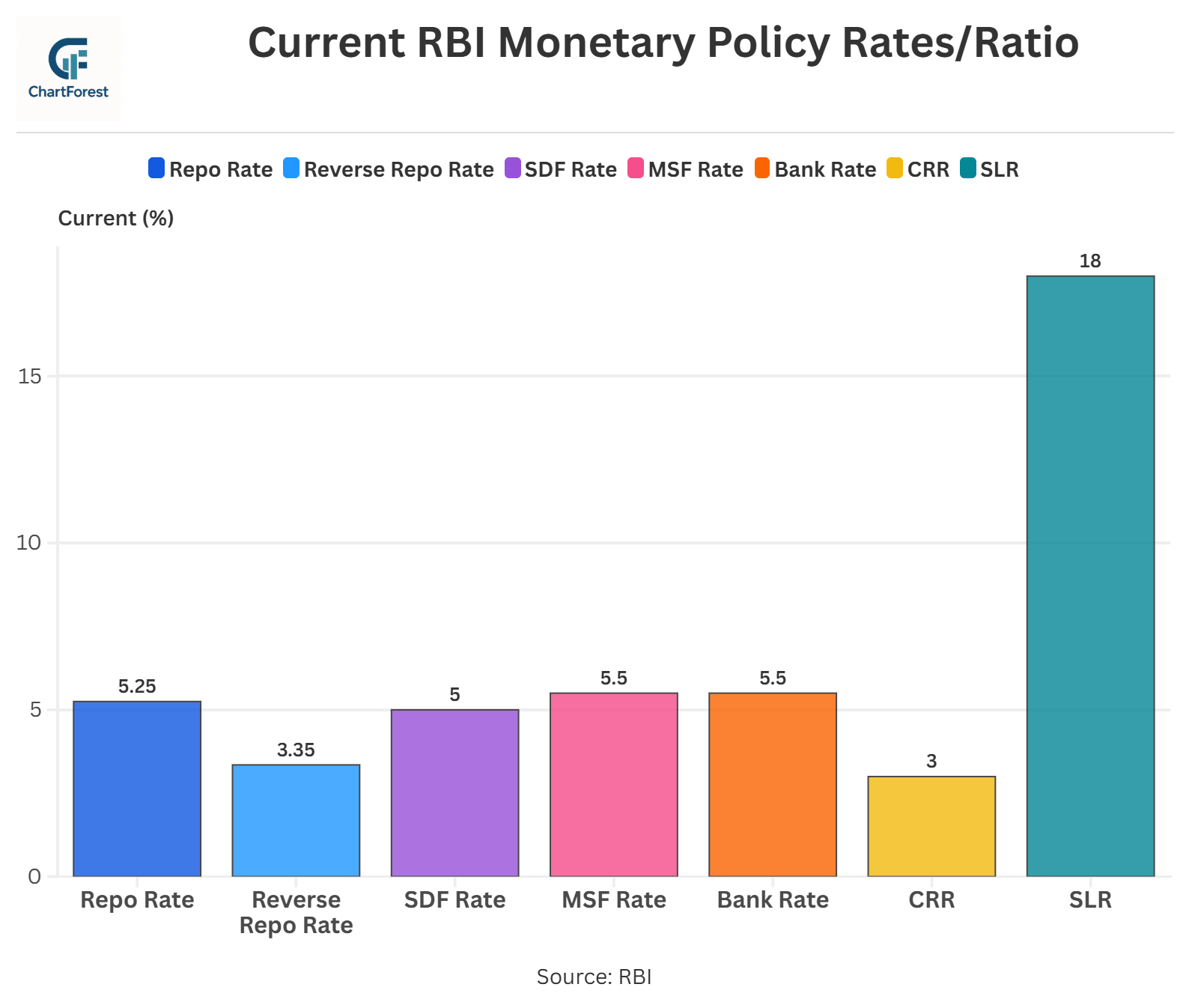

- During its 61st Monetary Policy Committee (MPC) meeting held from June 3 to 5, 2026, the Reserve Bank of India did not announce any changes to the Statutory Liquidity Ratio (SLR), indicating continuity in the existing regulatory liquidity framework for banks.

- The policy focused on maintaining the repo rate at 5.25%, while the Standing Deposit Facility (SDF) rate remained at 5.00% and the Marginal Standing Facility (MSF) rate and Bank Rate remained at 5.50%.

- The absence of any SLR-related announcement suggests that the RBI remains comfortable with the current liquidity buffer requirements maintained by banks.

- SLR continues to play an important role in ensuring that banks hold adequate liquid assets, such as government securities, cash, and gold, thereby strengthening the resilience of the banking system.

- The RBI emphasised growing global risks, including elevated energy prices, supply-chain disruptions, financial market volatility, and uncertainty arising from the prolonged West Asia conflict.

- Rather than making changes to structural liquidity requirements such as the SLR, the RBI continues to rely on monetary policy tools and market operations to manage liquidity conditions and support financial stability.

- The meeting was chaired by RBI Governor Shri Sanjay Malhotra, with members Dr Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr Poonam Gupta, and Shri Indranil Bhattacharyya in attendance.

- The decision reflects the RBI’s broader approach of maintaining regulatory stability while closely monitoring inflation, growth, liquidity conditions, and external risks facing the economy.

Reasons the RBI Left the SLR Framework Unchanged

Adequate Liquidity Buffers Already Exist: The RBI appears comfortable with the existing liquidity buffers maintained by banks. Since banks are already holding sufficient liquid assets, there was no immediate need to alter the SLR framework.

Focus on Monetary Policy Rather Than Regulatory Changes: The June 2026 policy meeting was primarily focused on interest rate decisions, inflation risks, and economic growth. As a result, the RBI chose not to introduce changes to long-term regulatory requirements such as the SLR.

Supporting Banking System Stability: Keeping the SLR framework unchanged helps maintain stability in banks’ balance sheets and investment portfolios. Sudden changes to liquidity requirements could force banks to adjust their holdings of government securities and other liquid assets.

Avoiding Unnecessary Operational Adjustments: Changes to the SLR can require banks to modify treasury operations, liquidity management strategies, and investment allocations. By leaving the framework unchanged, the RBI avoids imposing additional operational burdens on financial institutions.

Allowing Banks to Focus on Credit Growth: An unchanged SLR framework enables banks to continue supporting credit demand without having to adjust their asset allocation strategies. This helps maintain a balance between financial stability and the flow of credit to the economy.

Reliance on Flexible Liquidity Management Tools: The RBI has several market-based tools available to manage liquidity conditions, including the Liquidity Adjustment Facility (LAF), open market operations (OMOs), and foreign exchange operations. These instruments provide greater flexibility than changes to structural regulatory ratios.

Preserving Confidence During Global Uncertainty: With global risks rising due to higher energy prices, supply-chain disruptions, and geopolitical tensions, maintaining the existing SLR framework provides stability and predictability for banks and financial markets.

Maintaining Regulatory Continuity: The absence of any SLR-related announcement reflects the RBI’s preference for regulatory continuity while it evaluates evolving economic and financial conditions. This allows policymakers to monitor developments without introducing additional structural changes to the banking system.

Expected Effects of an Unchanged SLR Framework

- Continued Financial Stability: An unchanged SLR framework helps ensure that banks continue to maintain adequate holdings of liquid assets. These liquidity buffers strengthen the resilience of the banking sector during periods of market stress or economic uncertainty.

- Stable Demand for Government Securities: Since banks are not required to adjust their statutory liquidity holdings, demand for government securities is likely to remain broadly stable. This supports the orderly functioning of the government bond market.

- Predictability in Bank Treasury Operations: Banks can continue managing their investment portfolios and liquidity positions without making significant adjustments to comply with new regulatory requirements. This improves operational certainty and planning.

- No Disruption to Asset Allocation Strategies: Changes in the SLR can influence how banks allocate funds between loans and liquid assets. By leaving the framework unchanged, the RBI allows banks to continue executing their existing balance-sheet and investment strategies.

- Support for Long-Term Liquidity Resilience: The SLR serves as an important safeguard by ensuring that banks maintain a stock of high-quality liquid assets. An unchanged framework helps preserve this protective buffer within the financial system.

- Smooth Functioning of the Banking System: Regulatory stability reduces the need for banks to undertake sudden portfolio rebalancing or liquidity adjustments. This contributes to the smooth functioning of banking operations and financial intermediation.

- Greater Focus on Credit and Business Growth: Without changes to statutory liquidity requirements, banks can focus on meeting credit demand, expanding business activity, and supporting economic growth rather than adjusting to new regulatory obligations.

- Confidence for Financial Markets: The absence of changes to the SLR framework signals policy continuity and regulatory stability. This can support confidence among banks, investors, and other market participants during a period of heightened global uncertainty.

RBI Statutory Liquidity Ratio (SLR): Historical Chart

Statutory Liquidity Ratio (SLR) - Historical & Current Trends

RBI Monetary Policy Rates & Ratios

About RBI Statutory Liquidity Ratio (SLR)

Overview – SLR stands for Statutory Liquidity Ratio. The SLR means that the commercial banks have to maintain a specific percentage of their deposits in liquid assets, primarily government securities, gold, and cash.

Importance of Statutory Liquidity Ratio (SLR) –

Maintaining liquidity: Similar to the Cash Reserve Ratio (CRR), the main goal of the SLR is to maintain liquidity in the banking system.

Preventing liquidation when CRR hikes: It also prevents commercial banks from excessively liquidating their liquid assets when the RBI raises the CRR.

Investment in govt securities: SLR inherently requires banks to invest a portion of their deposits in government securities.

Maintain credit flow: SLR is used by RBI to maintain credit flow into the banks.

Control inflation: When inflation goes up, the RBI increases the SLR. It forces the banks to allocate more funds to govt securities, thereby reducing the amount of money circulating in the economy and potentially curbing inflation. Conversely, reducing SLR increases liquidity with banks, which can stimulate economic growth.

FAQs

SLR is a rule set by the RBI that requires banks to keep a certain percentage of their total deposits (NDTL) in liquid assets like cash, gold, or government-approved securities.

CRR is the portion of cash that banks are required to keep with the RBI, and they don’t earn any interest on it. On the other hand, SLR is a reserve that banks maintain in the form of approved securities, like government bonds or gold, which can earn them returns. While CRR helps control liquidity, SLR plays a role in ensuring the bank’s stability and solvency.

When the RBI increases the SLR, banks are required to keep more liquid assets, leaving them with less money to lend and helping to manage inflation. On the other hand, lowering the SLR gives banks more room to lend, which can stimulate growth but needs to be carefully managed to avoid inflationary pressures.

The Statutory Liquidity Ratio, or SLR, is shown as a percentage of a bank’s Net Demand and Time Liabilities (NDTL). It’s worked out using a simple formula: SLR = (Liquid Assets / NDTL) × 100. Liquid assets cover things like cash, gold, and approved securities that the bank keeps on hand.

Related Indicators

Other Indicators

Inflation and Price Indicators

GDP & Economic Growth Indicators

Trade & External Sector Indicators

Business & Industrial Indicators

Consumer & Labour Market Indicators

Important

If you notice any discrepancies in the data or find any inaccuracies, please let us know. We will review and correct them as soon as possible.